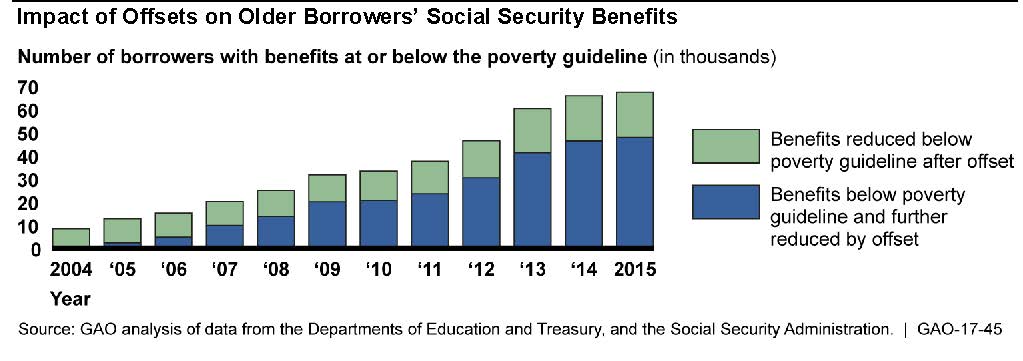

The Government Accountability Office (GAO) has issued a 90 page report on the offsets applied to Social Security benefits due to unpaid student loans. Even though the GAO seems to me to try to downplay the problem, it's still clear that it's real and serious. Many people are being thrown into poverty by the offsets as shown by the chart below, even though many of the student loans went to pay for nearly worthless online education.

|

| Click on chart to view full size |

11 comments:

And having a defaulted student loan (federal debt)will preclude an SSD/SSI applicant the opportunity to have their denial reviewed by federal court. so sad.

Kick them when they are down.

This is tragic.

Any poor person can get out of these offsets by signing up for Income Based Repayment. For a person "below poverty guidelines", this would bring their amount owed to $0/month and make the offset disappear.

People just don't know about it.

Howard, I have never heard that about loans defaulting and federal court. thanks for the info.

But white collar crime is faceless, nobody really gets hurt and we just pocket a little money....

As stated in your post "even though many of the student loans went to pay for nearly worthless online education." The question always remains, who is responsible for this outcome? And why should others pay for the poor choices/life decisions made by individuals? Of course, those going to well established colleges and universities are also facing the consequences of taking more than 4 years to complete their education, especially in coursework that, to be kind, does not lead to success based on any cost/benefit analysis.

@1:30

Your assertion that those who default on student loans due to disability are at fault as such a circumstance is a result of "poor choices/life decisions" is unreasonable.

Online universities were certified by the department of education and therefore eligible for federal loans.

In any event, ignoring the reference to online degrees which are generally worthless, debilitating brain injuries can result from cancer, assault, genetic defect, drunk driver, military service, just to name a few circumstances which are not a result of poor life choices or decisions.

But many unfortunate things happen to lots of people in life. Things are not just poor choices because someone became disabled.

For instance, if someone buys a house they could afford while working full-time but them becomes disabled and can no longer pay the mortgage, should the loan against the home be discharged?

If you believe it should, then where does it stop? Car loans, student loans, personal loans...why stop? When someone is living below poverty levels, shouldn't any and all debt be forgiven?

1:30 PM This article is not about the loans, but, rather, the tax for loan forgiveness. The irony is that the loans would be deemed "uncollectable." However, if the loans are forgiven, the tax is not! This actually discourages qualified people from applying for the forgiveness.

10:47 PM. Where are people asking for house loans to be discharged? Asking for tax forgiveness with student loan forgiveness to the federal government is a far cry from asking for mortgage forgiveness!

Opps, I was thinking about the lump of coal as I was writing my comments!

The issue here is that time after time, Congress makes a law and fails to make allowances for inflation. The $750.00 amount that couldn't be touched has not been adjusted for inflation since the law was passed in 1996!

How did this happen??

I can tell you. When Bush II signed the 2005 Bankruptcy Reform Act is made SLs all but non-dischargeable. Prior to that point, they could be discharged upon showing a period of repayment status (first 5, then 7 years).

When that happened, the economic brakes were removed from the lenders. Non-dischargeable? Lend it all and to all comers! Unfettered money supply? No wonder education costs have sky-rocketed. Scam educational entities? Naturally.

For perspective, consider that IRS tax debt is dischargeable after 3 years.

Student loans....Never.

@ Matt

I took bankruptcy in LS from an adjunct who still is a prominent practicing attorney in the area. He would regularly rail on the W admin and that Congress for "bap-see-puh" and the huge toll it took on debtors.

To answer 10:47--yes, every debt should be dischargeable at a certain (not too hard to meet!) point. Keeping folks in debt is inhumane and creates near-indentured servitude, and lordy knows major credit institutions, etc. are perfectly well-suited to handle those losses. It's easy as pie to discharge CC debt and yet VISA, et al continue to rake in money hand over fist (with the only dips experienced in recent years due to consumer protection laws minimizing swipe fees and downward pressure on those fees thanks to Square, Apple Pay, etc.).

The bankruptcy rules as currently existing are yet another example of socializing the costs (almost exclusively on middle class or poor) and privatizing the rewards.

Post a Comment